Following a couple of robust earnings reports, investors are eagerly anticipating Nvidia’s (NASDAQ:NVDA) upcoming quarterly update on Tuesday, November 21, for the fiscal third quarter of 2023 (October quarter). Goldman Sachs analyst Toshiya Hari foresees another positive statement from the chip giant, expressing confidence in strong FY3Q results, FY4Q guidance, and optimistic commentary from management that aligns with their bullish outlook on the stock.

Nvidia, leveraging its superior Data Center products, has capitalized on the 2023 AI revolution. Hari predicts that the upcoming report and FY4Q outlook will highlight the ongoing shift in wallet share towards accelerated computing (i.e., GPU) at the expense of general-purpose compute (i.e., CPU) in the company’s core Data Center segment.

Analyzing the changing expectations for Nvidia on the Street this year reveals a notable trend. Year-to-date, analysts have substantially raised their revenue projections for Nvidia’s Data Center segment in 2023 by 122%, soaring from $18 billion to $39 billion. In contrast, revenue expectations for AMD‘s Data Center segment have decreased by 20%, dropping from $8.2 billion to $6.6 billion, as have Intel’s Data Center & AI segment expectations, declining by 14% from $18.3 billion to $15.6 billion.

While Hari anticipates a slowdown in the acceleration of computing adoption and envisions a modest increase in 2024 spending on traditional computing, particularly among cloud hyperscalers, he believes accelerators will continue gaining market share over the medium to long run. This projection is based on the proliferation of AI across various sectors and the increasing complexity of data center workloads.

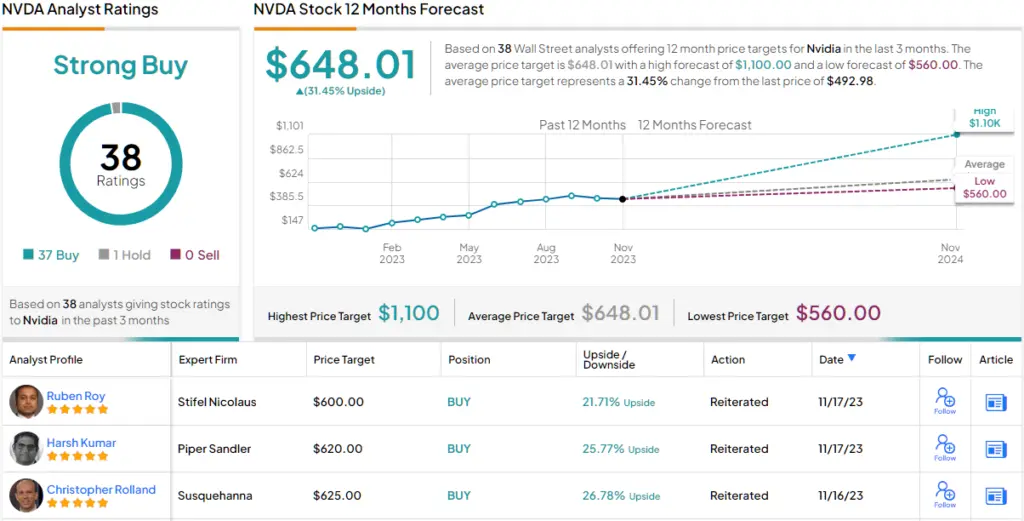

Given Nvidia’s robust hardware and software offerings, coupled with its rapid pace of innovation, Hari is confident in the company maintaining its position as the “industry standard.” Despite a 207% year-to-date increase in shares, Hari emphasizes Nvidia’s attractive risk/reward profile and recommends a Buy rating, setting a $605 price target with a potential upside of 24% from current levels.

Supported by 36 of Hari’s colleagues who share a bullish sentiment, the consensus rating leans heavily towards Strong Buy, with an average target of $648.01, suggesting a 31% climb in shares over the coming months.