What Traders Need to Know

At the start of April 2025, the global trade war sharply escalated with a new wave of reciprocal tariffs between major economic powers. The United States triggered this round by announcing unprecedented tariffs targeting both allies and rivals alike, prompting swift responses from China and others.

These fast-paced developments shook global financial markets. Stock indexes, commodity prices, and currencies fluctuated wildly with each announcement. Below is a detailed timeline of events from April 1 to 15, followed by an analysis of market impacts, policy motives, and warnings based on the views of experts and international institutions.

The Latest Escalation in the Trade War: A Timeline of Events

April 2, 2025

The United States Launches a Comprehensive Tariff Attack:

U.S. President Donald Trump announced the imposition of “reciprocal” tariffs on most countries worldwide, with a minimum rate of 10%. The new tariffs included a 25% levy on European imports of cars, steel, and aluminum, and 20% on nearly all other goods from the European Union, alongside 26% on Indian imports and other countries.

The administration described this move as a means to protect American industries and achieve “fairness” in trade. The decision caused widespread shock, as the U.S. Treasury Secretary stated that trade partners—including allies—had not made sufficient concessions, leading to this unilateral action aimed at gaining negotiation leverage. Domestically, early April data showed increasing pressure on U.S. consumers and industries reliant on imported inputs. Ursula von der Leyen, President of the European Commission, warned that these American tariffs would impose “heavy costs on consumers and businesses inside the United States” and inflict significant damage on the global economy.

April 4, 2025

China Responds in Kind:

The People’s Republic of China became the first country to directly retaliate against Trump’s new tariffs. On this Friday, Beijing imposed a 34% tariff on all U.S. goods, alongside strict restrictions on the export of strategic rare earth metals to the U.S. This Chinese response was seen as “retaliatory” and a significant escalation, exceeding expectations both in scope and intensity. Chinese officials described the U.S. tariffs as a “unilateral bullying act,” emphasizing that China would not tolerate violations of its sovereignty and developmental interests. Financial markets immediately sensed the danger, and global stock exchanges experienced panic, with investors growing concerned about the two largest economies in the world sliding into a full-scale trade war.

April 5, 2025

U.S. Tariffs Come into Effect Globally:

On this date, the U.S. broad 10% tariffs on most imports from countries around the world took effect. Despite objections from allies, Washington pressed ahead with implementing these extensive tariffs.

Emerging markets, particularly in the Asia-Pacific region, experienced significant turmoil, as their economies—heavily exposed to U.S. demand—were especially vulnerable to these tariffs. However, White House documents revealed that temporary exemptions could be granted to certain partners. Trump’s order included a 90-day grace period for countries taking “concrete” steps to address trade imbalances with the U.S. Many allies seized this opportunity to negotiate; countries like Indonesia and Taiwan announced they would not retaliate with similar measures but would stick to diplomatic solutions, while India quickly sought an early agreement with Washington to avoid escalation.

Indeed, India confirmed it would not impose counter-tariffs on U.S. imports, which were taxed at 26%, citing ongoing negotiations aimed at reaching a trade agreement by Fall 2025. The Indian government, led by Narendra Modi, also took steps to win Washington’s favor, such as reducing tariffs on U.S. luxury motorcycles and bourbon, and removing the digital services tax targeting major U.S. tech firms.

April 7, 2025

New Threats and European Efforts for De-escalation:

After a weekend filled with statements, Trump emerged on Monday, April 7, waving another leverage card. He threatened to impose additional 50% tariffs on China if it did not immediately reverse its latest retaliatory tariffs.

This public warning followed a closed meeting at the White House where Trump’s economic team assessed the lack of de-escalation signals from Beijing. Meanwhile, Europe intensified its diplomatic efforts to avoid further expansion of the conflict.

In Brussels, Commission President von der Leyen stated that the European Union was ready to negotiate with Washington, even offering a “zero for zero” initiative to eliminate all reciprocal tariffs on industrial goods. She confirmed that this offer remained on the table, but it was conditional on the U.S. stepping back from escalation. She also highlighted that the EU was prepared to take countermeasures to defend its interests if negotiations failed, including protecting Europe from the side effects of shifting global trade routes.

At the same time, EU trade ministers agreed to prioritize dialogue with Washington over immediate retaliation in a bid to contain the crisis. Amid these efforts, stock market indicators, including those on Wall Street, fluctuated with every new leak or statement, as investors awaited any sign of a breakthrough in negotiations between the U.S. and its partners.

April 8-9, 2025

Unprecedented Escalation in U.S. Tariffs:

By the evening of April 8, in the absence of de-escalation signals from Beijing, Trump followed through on his threat and raised tariffs again on Chinese imports. In a surprise move, Washington added 50 percentage points to its tariffs on China, bringing the cumulative tariff rate on Chinese goods to 104% starting April 9.

The White House confirmed that this substantial increase would remain in place “until China reaches a fair trade agreement” with the United States. This escalation was a direct response to China’s refusal to reduce its 34% tariff on U.S. goods.

At the same time, the U.S. administration unveiled a dual strategy: intensifying pressure on China while temporarily suspending some of the new tariffs for 90 days on a number of allied countries. This provided partners like the European Union, Canada, and Mexico an opportunity to negotiate during this grace period instead of immediately engaging in a trade confrontation.

This move contributed to a relative calm in markets regarding U.S. allies but further isolated China economically. In response, the Chinese Ministry of Finance announced on the morning of April 9 that it would raise additional tariffs on U.S. products to 84%.

Chinese officials described this decision as defensive and retaliatory in response to the U.S.’s latest tariff increase. A Chinese foreign ministry spokesperson emphasized that China would “continue to take decisive and effective measures to protect its legitimate rights and interests,” stressing that China would not succumb to external pressures or threats.

As these tariff hikes exchanged rapidly, global markets plunged into sharp volatility, with the Dow Jones Industrial Average losing over $5 trillion in stock value over two days due to the panic triggered by these developments.

April 10, 2025

Consolidating the U.S. Position and Partial Relief on Some Tariffs:

On April 10, the U.S. administration clarified the details of the new tariff structure. The White House confirmed via CNBC that the cumulative tariff rate on China had actually reached 145% after the latest increase.

This figure includes a new 125% tariff on Chinese goods in addition to the previous 20% tariff imposed earlier this year in response to the fentanyl crisis.

Thus, U.S. tariffs on all Chinese imports reached an unprecedented level. At the same time, Washington sought to mitigate some of the negative effects on U.S. consumers and the tech sector. The U.S. Customs and Border Protection announced that smartphones, computers, and certain consumer electronics would be exempt from the new tariffs, as most of these goods are imported by U.S. companies from China.

This exemption was seen as a tactical retreat by Trump from a broader tightening, as analysts noted that the exemption of electronics and the White House’s hints at potentially easing car tariffs provided some relief to risk assets such as oil and stocks.

On the other hand, Trump suggested on the same day that he might reconsider the 25% tariff on car imports and auto parts from Canada, Mexico, and other countries, signaling an attempt to reassure U.S. allies under the USMCA agreement and avoid opening a new front in the trade war.

Despite this partial easing, the White House confirmed the continuation of the 25% tariffs on certain goods from Canada and Mexico not covered under the North American Free Trade Agreement, as well as a 10% tariff on all other imports worldwide. This fluctuating trade policy led OPEC to reduce its global oil demand growth forecast for the first time since December, amid fears of a global economic slowdown due to the trade war.

April 11, 2025

New Chinese Response and WTO Escalation:

On Friday, April 11, China announced an additional escalation in its countermeasures. Beijing raised tariffs on U.S. imports to 125% starting Saturday, April 12, up from the previously disclosed 84%.

This move was a direct response to Trump’s unprecedented tariff increase on China. The Chinese government stated it would “ignore” any future U.S. tariff hikes, signaling its refusal to bow to further extortion.

In addition, China filed a formal complaint with the World Trade Organization (WTO) against the new U.S. tariffs, considering them a severe violation of international trade rules. In a strong statement, the Customs Tariff Committee of the Chinese State Council declared that the U.S.’s imposition of “abnormally high” tariffs on China violated fundamental economic laws and blamed Washington for the sharp disruptions to the global economy caused by this trade war.

Meanwhile, global markets reacted differently to these developments. After a sharp decline earlier in the week, gold prices surged as investors flocked to safe havens, while oil prices began to stabilize due to the U.S. exemptions and China’s recovery in crude imports.

However, in general, a sense of caution and uncertainty remained dominant in financial and currency markets, as traders waited for the next developments in this round of the trade dispute.

April 15, 2025

International Reactions and Warnings at the Height of the Crisis:

By mid-April, the political rhetoric surrounding the trade war had intensified. In Hong Kong, Xia Baolong, Director of the Hong Kong and Macau Affairs Office in China, described the U.S. tariffs as “extremely rude and aimed at destroying Hong Kong,” suggesting that Washington was using the trade war as a political lever against China on issues beyond trade.

In Washington, the U.S. Treasury sought to reassure the markets by emphasizing its openness to a “fair deal” with China if it offered tangible concessions. At the same time, international institutions and economic experts began raising alarms.

JPMorgan, one of the largest investment banks, raised the likelihood of a recession in the U.S. and globally to 60% due to the tariffs, warning that they “threaten to undermine corporate confidence and slow global growth.” Goldman Sachs CEO David Solomon also warned of increasing “uncertainty caused by the new tariffs” and the risk of entering a new quarterly economic environment. He indicated significant risks to both the U.S. and global economies, with the possibility of markets remaining “volatile until clarity emerges.”

Estimates from the International Monetary Fund and the World Bank suggested that continued escalation could cost the global economy hundreds of billions of dollars and reduce global growth significantly. There were growing concerns about inflation from the tariffs, as higher tariffs lead to increased prices for goods for the end consumer, which could force central banks to tighten monetary policies at an inopportune time. In this context, Reuters reported that the wave of U.S. tariffs had pushed consumer prices in Asia and Europe to new highs, while Asian currencies had depreciated under pressure from expectations of a slowdown in exports and investment.

The Impact of Developments on Global Financial Markets

This escalating trade war has had an immediate and profound effect on global financial markets, and its repercussions are of particular interest to traders and investors. Stock markets have been shaken since early April with every new development:

Stock Markets

U.S. and European indices suffered significant losses in the early days of the conflict. The S&P 500 Index dropped more than 4% during the first week of April, while the MSCI Emerging Markets Index entered a selling wave, losing all its gains for the year.

According to CNBC estimates, over 5.4 trillion dollars were wiped off the value of global stocks in just two sessions, driven by the panic caused by tariffs.

Industrial and technology stocks were particularly affected. For example, European car manufacturers faced selling pressure after being targeted with a 25% U.S. tariff, while Asian electronics companies saw their stock prices drop due to supply chain concerns.

On the other hand, markets took a breath after the U.S. announced exemptions for phones and computers from tariffs, leading to a rebound in tech stocks and a partial recovery in U.S. indices. Even Apple, the tech giant, saw a rise in its stock following the tariff exemptions. However, volatility remained dominant. Goldman Sachs experts described the situation as one where markets would remain volatile until the outcome of the negotiations becomes clearer or the contradictory decisions stop.

Indeed, we saw the Dow Jones index fluctuate within hundreds of points, rising and falling over just a few days depending on the news, making risk management a daily challenge for traders.

Commodity and Metals Markets

Investors clearly turned towards safe-haven assets in the face of uncertainty.

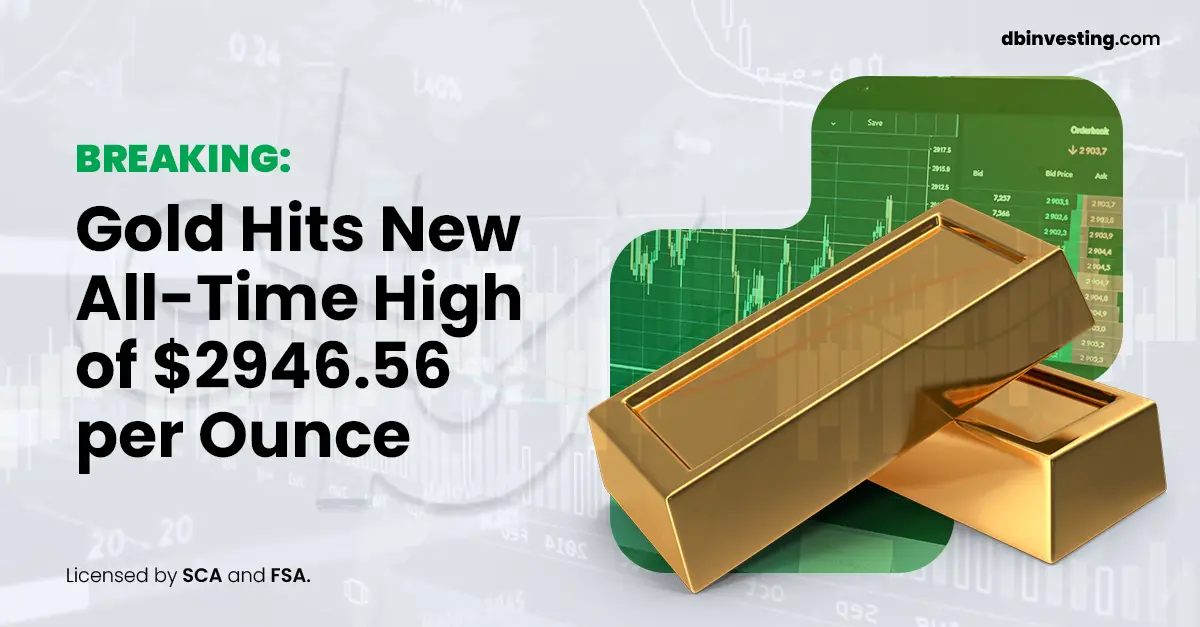

Gold regained its shine strongly, stabilizing near its highest recorded levels in mid-April. The price of an ounce reached around $3,211 after briefly touching a peak above $3,245 on April 14.

This level means that gold rose by more than 20% since the beginning of the year, driven by the intensifying trade war, which dampened global growth prospects and weakened confidence even in some traditionally safe U.S. assets.

On the other hand, crude oil prices were impacted by conflicting factors. Fears of a global economic slowdown put downward pressure on prices, while some temporary positive factors helped support them.

On April 15, Brent crude and West Texas Intermediate (WTI) oil prices rose slightly (~0.2%), reaching $65 and $61.7 per barrel, respectively. This was supported by two factors: Trump’s exemptions for some electronics from tariffs, which renewed hopes of avoiding a global energy demand hit, and a 5% increase in China’s oil imports in March on an annual basis, in anticipation of a decline in Iranian supplies.

With the announcement of the U.S.’s intention to grant exemptions from import tariffs on electronic products and reduce tariffs on cars, the oil market felt some relief, as this indicated a potential easing of the trade war, which could reduce the risk of falling fuel demand.

However, the OPEC organization, in a precautionary move, lowered its forecast for global oil demand growth for the first time since the end of last year due to the uncertainty created by fluctuating U.S. trade policies.

It is also worth noting that industrial metal prices, such as copper and aluminum, declined in early April due to expectations of damage to global industrial activity, before partially recovering as talks of potential negotiations between Washington and Brussels emerged. In general, commodity traders found themselves facing a complex situation: a trade war dampening global demand on one hand, and actions and expectations increasing hopes on the other.

Currency Market

Global exchange rates were marked by clear fluctuations as risk appetite shifted.

Safe-haven currencies like the Japanese yen and the Swiss franc rose sharply in early April as investors rushed toward safety, while emerging market currencies faced selling pressure amid fears of capital outflows.

The U.S. dollar fell below the 100 level on its main index (DXY) by mid-month, influenced by expectations that tariffs could slow the U.S. economy and potentially prompt the Federal Reserve to ease its monetary policy.

In contrast, the Chinese yuan dropped to its lowest level in six months, reflecting efforts by currency markets to counter the impact of tariffs by devaluing the Chinese currency – a move that could somewhat alleviate the burden of tariffs on Chinese exports.

The euro and British pound also saw volatility, pressured by concerns over European exports being affected by Trump’s tariffs. However, they received relative support as the European Union showed unity in negotiations and better-than-expected European data helped reduce fears temporarily.

David Solomon, CEO of Goldman Sachs, mentioned that there is “massive activity in the currency market right now” as investors focus on the U.S. dollar’s movements and the fluctuating situation.

This activity has created both opportunities and risks for currency traders. Sharp volatility means the potential for significant profits for those who manage timing and risks well, but it also carries high risks of substantial losses if events reverse suddenly.

Conclusion

Overall, the trade war quickly reflected in the mood of global markets: uncertainty reached rare levels, and daily fluctuations in asset prices were enough to confuse even seasoned investors. Traders have been closely monitoring every statement or move from Washington, Beijing, and Brussels, as political news can instantly turn into price movements on financial platforms.

Investors are now hoping for signs of progress in negotiations between the U.S. and the countries that had tariffs suspended for 90 days, as any indication of an agreement would immediately translate into market relief and increased risk appetite.

Economic Analysis and Motivations Behind the Policies

The recent escalation in the trade war can be explained by several economic and political motivations from the various parties involved:

U.S. Motivations

The Trump administration adopted an aggressive stance in trade, driven by several considerations. The first of these was reducing the U.S.’s chronic trade deficit with countries such as China, Germany, and Mexico. Trump believes that imposing tariffs will encourage the relocation of industries back to the U.S. and reduce the import of cheap goods.

Secondly, there are demands related to intellectual property and forced technology transfer. Washington is pressuring Beijing to change practices it deems unfair to American companies, such as forcing them to transfer technology to Chinese partners.

Thirdly, geopolitical and security reasons have entered into the trade equation. The Trump administration has publicly linked tariffs to non-commercial issues. For example, the imposition of an additional 20% tariff on China was justified as a response to Beijing’s role in the U.S. drug crisis (the fentanyl issue). Washington also hinted that China’s stance on issues like Hong Kong and Taiwan could be part of the broader trade pressure.

Additionally, Trump seeks to renegotiate international trade agreements (such as replacing NAFTA with the USMCA) to secure terms he believes are fairer to the U.S. Naturally, policymakers in the White House are aware of the domestic costs of these tariffs, as they effectively serve as taxes on American consumers by raising the prices of many products. However, the administration’s gamble was that the pain experienced by the trade partners would outweigh the pain felt in the U.S., eventually forcing them to make substantial concessions.

The CEO of Goldman Sachs has praised the administration’s focus on removing trade barriers and enhancing America’s competitiveness, though he warned of the risks of this approach. This reflects the divide in American business opinions: some see the need to stand firm against “unfair trade practices” that have been in place for decades, while others caution that this tariff gamble could backfire by weakening growth, increasing inflation, and pushing the economy into a recession.

China’s Motivations

China has adopted a firm stance in response to U.S. pressures, based on both economic and sovereignty considerations.

From an economic perspective, Beijing is keen to protect its export-based growth model. A restrained response might be interpreted as weakness, which could encourage Washington to make further demands. Moreover, China has limited tools to counteract the impact of tariffs (such as devaluing the yuan or supporting exporters), so it has chosen a robust response to deter the U.S. from continuing its escalation.

Additionally, China seeks to buy time to find alternative markets and suppliers while adjusting its supply chains to the new situation.

From a sovereignty standpoint, Chinese leadership sees Washington’s actions as an attempt to contain its rise and disrupt its ascent to becoming a global technological power (especially with America’s investigations into semiconductor and pharmaceutical imports aimed at imposing new tariffs). National dignity also plays a significant role; Chinese officials have made it clear that their people “do not cause trouble but are not afraid of it,” and that pressure and coercion are not the right way to deal with China.

China also understands that the U.S. economy itself will suffer from the trade war, so it may bet on its strategic patience and on domestic pressure within the U.S. (from the business sector or consumers) to rein in Trump. Therefore, China’s goal is to avoid making significant concessions under direct pressure and to wait for more balanced negotiating conditions, whether through bilateral talks or within multilateral frameworks like the World Trade Organization (WTO).

China has openly accused the U.S. of attempting to “coerce” it economically, describing Trump’s strategy as a “bad joke,” implying its ineffectiveness against a massive and diversified economy like China.

European Union, Russia, and Other Countries’ Positions

For Europe, the primary motivations are protecting its industrial interests and free trade. Europeans are displeased with being included in the same targeting group as China, especially since they share many of Washington’s criticisms of Chinese practices.

Thus, Brussels tries to balance between de-escalation and firmness: it offered a “zero tariff” deal with the U.S. in an attempt to defuse the crisis, but at the same time, it prepared a list of countermeasures valued at nearly €26 billion to target U.S. imports if necessary.

Europe recognizes that a comprehensive trade escalation with the U.S. will hurt both sides significantly (especially major European industries like the German automobile sector), so it preferred a negotiator-first approach. By showing willingness to remove non-tariff barriers (such as certain regulatory measures), Europe sends a signal to Trump that there are ways to address his trade concerns without engaging in a trade war.

In contrast, Peter Navarro, the White House trade advisor, attempted to complicate matters by insisting that Europe itself must remove its 19% value-added tax and lower food safety standards, among other demands, if it wants to reduce U.S. tariffs, creating difficult conditions for reaching a comprehensive agreement.

As for Russia, although it is less directly involved (due to existing Western sanctions and a decline in its trade with the U.S.), it benefits strategically from the U.S.-China dispute, as it diverts Washington’s and Beijing’s attention. Moscow has openly supported Beijing’s position against “American hegemony” in the global trading system, viewing the growing China-Russia alliance as an opportunity to build an economic block facing Western pressures.

Moreover, Russia may benefit from China’s search for alternative suppliers (for example, increasing energy and agricultural purchases from Russia to offset U.S. imports). However, Moscow has been indirectly affected by the decline in oil prices and their volatility due to expectations of a global growth slowdown.

For other Asian countries like India, Brazil, and Southeast Asia, they are trying to seize opportunities and avoid harm simultaneously. India— as mentioned earlier—has chosen a negotiation approach to improve its trade deal with the U.S. (such as reducing tariffs on certain U.S. goods in exchange for exemptions), and it may benefit from the tension between Washington and Beijing by attracting some investments or increasing its agricultural exports to China.

Countries like Vietnam and Taiwan may experience shifts in supply chains as multinational companies look for alternatives to China to avoid tariffs, which could benefit them in the long term. However, they are also at risk in the short term from reduced global demand and disrupted trade.

In general, economies not directly involved in the conflict are attempting to remain relatively neutral and capitalize on any trade diversion in their favor, while warning that they may have to act if they are harmed.

Fitch Ratings has pointed out that the increase in U.S. tariffs threatens the credit ratings of many Asia-Pacific countries due to their large exposure, although the 10% tariffs on most countries were less severe than the worst-case scenarios previously assumed by the agency.

Expected Macroeconomic Impacts

Most experts agree that continued escalation without resolution will negatively impact global economic growth. High tariffs mean increased production costs for companies (those importing raw materials or parts), which may prompt them to raise the prices of final products, reduce profit margins, or even delay investment plans.

This situation undermines global business confidence, as noted by JPMorgan, and makes executives more cautious in hiring and expanding. The International Monetary Fund (IMF) has warned that these major trade tensions could lead to sharp corrections in global stock markets and volatile currency fluctuations if unresolved.

As uncertainty rises, households typically delay major purchases, and businesses hold back on capital expenditures, weakening overall demand. Indeed, major investment banks like Goldman Sachs and Bank of America have raised their forecasts for the possibility of a recession in the coming year.

Economic models show that the trade war between the U.S. and China alone could reduce global economic growth by about 0.5 to 0.8 percentage points over two years, due to a decrease in trade and investment volumes. It also leads to an inefficient redistribution of resources, as companies are forced to reorganize supply chains at high costs, and some industries may relocate from low-cost locations to higher-cost but less politically risky sites, which means higher global commodity prices.

Of course, the final consumer will pay part of the price: tariffs are essentially an indirect tax, so inflation rates are expected to rise, especially in the U.S. (where many consumer goods are imported from China). Economic reports have indicated that Trump’s recent tariffs threaten to ignite inflation and push the global economy toward the edge of a recession unless addressed through agreements.

On the other hand, some argue that trade pressure may lead to a more balanced trading system in the long term if new agreements are reached. For example, China might open its financial and agricultural markets more to American investors and exporters to placate Washington’s anger, and major industrial nations might agree to reform the World Trade Organization and address issues related to industrial subsidies and forced technology transfer. However, these potential positive outcomes are still uncertain and fraught with political complexities.

Warnings and Future Expectations

In light of these developments, serious warnings and varying predictions have been issued regarding the near future of the global trade war:

Warnings from Experts and International Institutions

The International Monetary Fund (IMF) in its latest report warned that the continuation of the current trade escalation poses a “significant risk” to the global economy and could lead to a global recession scenario if trust erodes and investment shrinks. IMF Managing Director Kristalina Georgieva confirmed that the direct outcomes of this trade war would be rising inflation, declining economic growth, and possibly recession if not addressed.

The World Trade Organization (WTO) also expressed significant concern. WTO Director-General Ngozi Okonjo-Iweala stated that the recent U.S. actions could undermine the multilateral trade system and encourage other countries to adopt similar policies, threatening to dismantle the rules that have governed global trade for decades.

In addition to the IMF and WTO, major investment banks have raised the likelihood of a recession (JPMorgan 60%, Goldman Sachs 45%) and started outlining difficult scenarios for the markets:

HSBC described the forecast for China’s growth in 2025 as the “bleakest,” while Fitch warned of possible credit rating downgrades for several countries if tensions persist and result in financial expansion or significant export declines.

These institutions fear a vicious cycle: Tariffs → Rising prices → Declining demand → Economic slowdown → Financial instability → More protectionist measures as a political response.

Therefore, clear calls have been made to avoid this cycle: The Organisation for Economic Co-operation and Development (OECD) urged all parties, via a special statement, to exercise restraint and return to the negotiation table, as the only beneficiary of an extended trade war “will be no one.”

Future Predictions for the Trade War Path

In the short term (3-6 months), analysts predict that the situation will remain tense, with the possibility of partial negotiations. The United States and its allies (EU, Japan, Canada, Mexico, etc.) have a 90-day window (until early July 2025) to reach trade agreements to avoid reactivating suspended tariffs.

There is cautious optimism that this period may see mutual concessions: For example, Washington could indefinitely postpone the 10% tariffs on Europe if Europe agrees to reduce some regulatory barriers and increase imports of U.S. energy.

U.S.-India talks are also expected to continue, aiming for a breakthrough before Prime Minister Modi’s anticipated visit to Washington in the fall, seeking a mini-trade deal to resolve the dispute over the 26% tariffs.

On the other hand, the U.S.-China path appears more complicated. As of mid-April, there were no signs of high-level negotiations resuming between the two; in fact, fiery rhetoric from both sides only strengthens the impression that the divide has widened.

However, a sudden diplomatic breakthrough is not ruled out, perhaps through third-party mediation or an unplanned meeting between President Trump and Chinese President Xi Jinping during an international summit, especially if economic losses start to show clearly in either country’s economy.

Possible Scenarios for De-escalation

One potential de-escalation scenario is for Washington and Beijing to agree on a new ceasefire that restores tariffs to pre-April levels in exchange for China committing to a significant increase in imports of U.S. goods (such as energy and agriculture) during 2025-2026, with further structural reforms to be discussed later. This scenario is supported by the urgent desire for stability in the markets but requires flexible political will that may not be easily available in the current polarized environment.

Possibilities of Further Escalation

If diplomatic efforts fail, we could see further escalation after the 90-day period ends. The United States has threatened to impose tariffs on imports of semiconductors and medicines, sectors that are highly sensitive to global trade.

Trump’s expected announcement of a new tariff rate on imported semiconductors in the last week of April could ignite a wider technological confrontation.

China, for its part, has non-traditional weapons it could resort to if the war continues, including restricting exports of rare minerals vital for U.S. industries (something it has started to hint at) or even further devaluing the yuan to offset the effects of tariffs, though this could provoke more U.S. anger.

Additionally, Beijing may tighten its grip on the operations of U.S. multinational companies operating in China as a form of pressure (through regulatory delays or informal boycott campaigns).

On another front, internal political factors could also fuel escalation: As the U.S. enters the 2026 presidential election cycle, Trump may view hardening trade positions as a means of rallying his electoral base under the banner of protecting American workers. Similarly, Chinese leadership is unlikely to show any weakness to its people or neighbors.

In general, the current phase is characterized by a high degree of uncertainty. Experts advise investors and traders to be cautious and hedge against volatility, as political news has become the primary driver of markets in the short term.

Moreover, corporate planning has become challenging, as investment decisions depend on the outcome of these tariff battles. However, there is hope that the clear negative consequences will push all parties toward compromise. Given the new reality—”everyone is losing” as Bloomberg described it—economic pragmatism may eventually overcome the hardline rhetoric. Until then, the global trade war will remain the largest source of instability, with market makers closely watching whether the coming weeks will bring a negotiated breakthrough to end the escalation or whether we are headed toward a more intense phase of this unprecedented confrontation.